This post was originally published in [2021] and has been fully updated for 2026 with new data and tools.

In early 2026, Aave hit a record $100M in annualized net revenue, yet the token price remains stalled under $120.

Many investors are scratching their heads: Why AAVE token price isn’t following protocol revenue 2026 despite 60% market dominance?

The answer lies in the ‘Aave Will Win’ framework—a controversial $50M proposal that could finally link token value to protocol earnings

If you feel the DEFI industry will grow, then Aave can be a good investment! Aave does face the challenge of relying on Ethereum and has more people wanting to loan crypto than borrow it.

Keep reading, and I’ll share what makes Aave different than other DEFI projects. I’ll share the number 1 thing going for it, why crypto lending is better than traditional banking, and how to earn money with this project.

AAVE Value Gap Estimator (2026)

Is the $50M “Aave Will Win” proposal worth it?

Routes 100% of product fees to the DAO treasury.

*Calculated based on $1.6B Market Cap and 19.1% Staking Ratio (Feb 2026 Data).

Why the “Aave Will Win” Framework is the Catalyst for Token Re-Rating

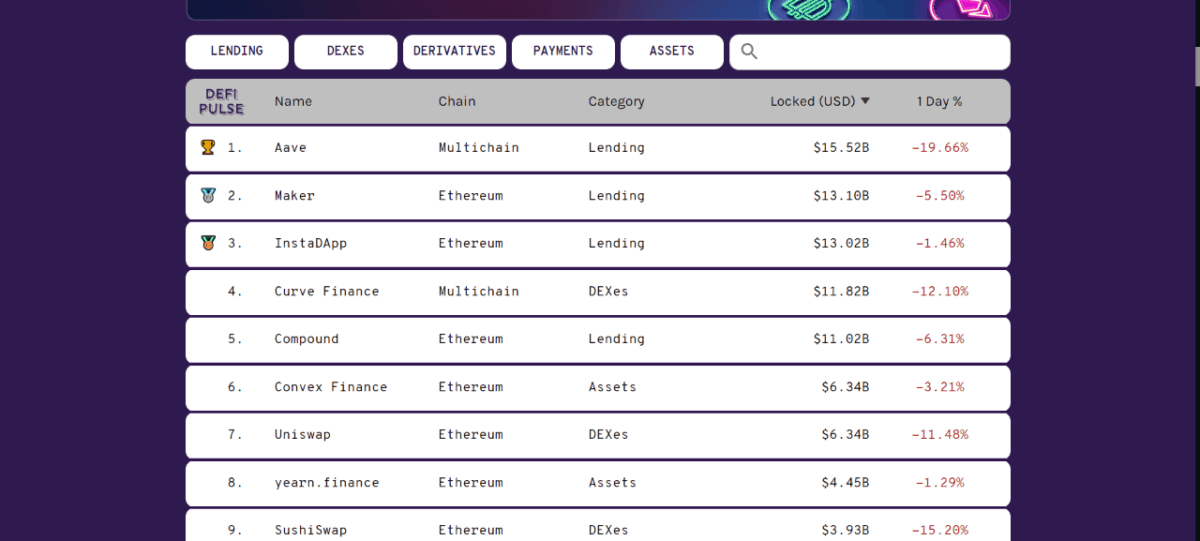

Aave dominates with 60% of the lending market and makes tons of money.

The protocol revenue is 100 million+.

You would think the token would shoot up, but it hasn’t.

The reason is that the AAVE system is a dual structure.

- Token holders collect fees from lending markets

- High margin revenue goes to Aave Labs

So, Investors became hesitant to buy the token if the most profitable stuff were seperate from the token.

In February 2026, as I’m writing this, Aave proposed something that could help.

100% of all the revenue Aave makes will go to the DAO treasury.

Then the AAVE token will change from governance only to a value-backed asset. Next, Aave Labs will transfer all trademarks and IP to a new Aave Foundation, ensuring the investors own the brand.

This whole change is called Aave Will Win.

Aave V2 vs. V4: How the “Hub and Spoke” Architecture Changed DeFi

In 2021, Aave was a bunch of isolated pools; in 2026, it was a liquid machine that was unified.

Aave V4 is rolling out in 2026 and this will allow the system to capture fees better.

The main change is the Aave Will Win idea, which, if implemented, can help the token price.

Is Aave a Bank? A Beginner’s Guide to the 2026 “Lending OS”

Aave is a decentralized lending project.

One of the great things about Aave is that there are NO annoying KYC requirements. KYC means (Know your customer), and means taking pictures of your ID (It’s a pain in the ass).

Oh, and if you want to go to a bank to borrow money, there is a big application, and it’s a (HUGE pain in the ass).

Aave is different due to its being on a blockchain, and it’s also built on Ethereum. The challenge with Ethereum is gas fees, and this means it can cost “a lot” to move things on the blockchain.

A second challenge with Ethereum is that it’s Turing complete, and this is a fancy way of saying MORE things can go wrong.

Aave was launched in 2017 and used to be called Eth Lend. In case you’re wondering what the hell Aave means (It’s a ghost from the language of Finland).

Aave does 3 things…

- You can borrow crypto

- You can lend crypto

- You can exchange tokens

If you wanted to borrow money from a traditional bank, there would be a big application, and you would need to have some collateral.

If you wanted to borrow money for a car, the bank would use the car title as collateral. If you didn’t pay back the loan, the bank would take the car.

With Aave, you would put crypto as collateral.

To ensure someone doesn’t borrow money and NEVER repay it (who would do that?), someone needs to put up more money in crypto than what they are borrowing.

Also, the prices of crypto can be crazy!

Someone can only take out 75% of the crypto that they put up for collateral. If someone puts up $100 worth of collateral, they can only borrow $75 dollars.

Aave also has LOTS of liquidity and, at the time of this blog post, is number 1 with DEFI (Decentralized Finance).

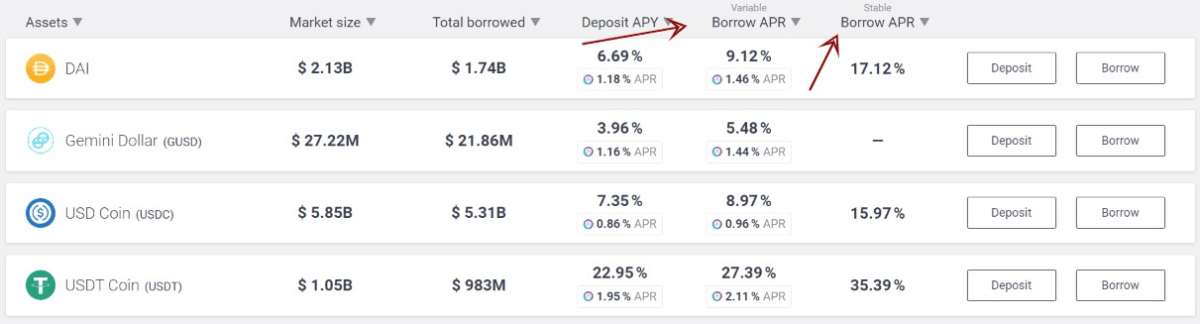

The interest getting paid comes from the borrowers who are paying to borrow crypto. The interest rate depends on the demand for that token.

If “many” people want to borrow a coin, then the interest on that coin will increase!

The interest rate someone can pay if they borrow is either Variable or Stable. Oh, and the stable rate can change if the market moves “a lot,” it’s just WAY more stable than the variable rate.

Aave has 29 ERC20 tokens (that I counted) at the time of this blog post. ERC20 stands for (Ethereum Request for Comment), and the 20 is just a random number.

Think of ERC20 as WordPress for Ethereum tokens, and it makes it easier for wallets and exchanges to accept the coin.

Many websites are built using WordPress, just like many Ethereum tokens are built with ERC20.

AAVE vs. stkAAVE vs. gAAVE: Which Token Has Better Yield?

The maximum supply of Aave is 16 million tokens compared to Bitcoin’s maximum supply of 21 million “this isn’t a lot.” The total supply of Aave in circulation is 12.5 million compared to Bitcoin’s 18 million.

A low supply is a good thing and does help the price.

Still, a low supply doesn’t mean anything if there is NO demand. What does the Aave token do?

One of the uses is for staking. If you’re not sure what staking is, you can check out this post HERE, where I do my best to simplify it.

If you stake the Aave token, you can get 5% returns; also, if something goes wrong with Aave, you can lose 30% of your investment.

The 30% penalty is both good and bad! Good because investors have more skin in the game, and bad because you can lose money.

Another way the token is used is for governance, and this means you can vote on where the project is headed.

Lastly, Aave tokens are used for discounts on borrowing fees, and someone can get their borrowing limit raised with the token.

How to Execute No-Code Aave V4 Flash Loans for Arbitrage

Flash loans are an interesting feature that charges 0.09% interest. Someone can take out a loan without any collateral. If someone doesn’t pay back the loan, then the transaction either gets reversed or canceled.

The catch is that it has to be in the same transaction.

The point of flash loans is so someone can borrow money to buy a token and resell it somewhere else, make money, and repay the loan in 1 transaction. (My head is exploding thinking about this)

It sounds crazy, but different exchanges usually have different prices for a token.

Another use for flash loans would be refinancing. You could borrow money with Aave to pay off debt and then transfer the money to get a “better” rate. You could do all this in 1 transaction.

Now, I do think borrowing money isn’t a good idea in general, but it’s an option!

It reminds me of the “Blue Light Special” that Kmart had a long time ago.

Basically, when the blue light special came on, and you were in the store, then you could save money buying an item. The sale usually lasted for around 15 minutes.

Best Chains for Aave V3 Liquidity Mining Rewards in 2026

Yes, Aave does have liquidity mining. When it comes to a DEX (Decentralized Exchange), you can exchange 1 token for another. The only way for this DEX to work is with a pool of money.

Nearly everyone is NOT going to deposit (money/crypto) into a pool without getting paid.

This is a WONDERFUL income-making opportunity!

What is cool about Aave is that they have a market to loan out the tokens, which you could get paid for, and this is called liquidity mining.

When it comes to stablecoins the yield would be between 4.78% to 13.49% + 3.5%. These rates, while good, I found this project HERE to pay a higher rate!

You can use the code 939517 for $30 in free coins if you make a deposit of over $50.

Also, I like the DEFI project because it’s based on Bitcoin and is “very” secure, plus I know the founders, and they have lots of nifty plans for the future.

(Truthfully, I’m a little biased)

Still, liquidity mining is a wonderful opportunity, with whatever project you go with.

Conclusion to Why AAVE token price isn’t following protocol revenue 2026

I’m extremely bullish on DEFI because it can do everything a bank can do faster, easier, and with fewer fees. Also, there is less overhead.

Paypal took over banking, and crypto is the next level. Heck, you might even say PayPal made Elon Musk the person he is by financing all his other projects.

Aave does have a lot going for it.

Still, nothing is perfect, and one of the weakest links in Aave is that, hopefully, Ethereum will be able to handle it.

Ethereum is going through MANY changes at the time of this blog post, and you can read some of them from the link HERE.

Another challenge with Aave is that the number of people wanting to earn interest from their crypto has increased a lot, while the number of people wanting to borrow crypto has stayed low.

Whether you’re into Aave, Defichain, or any other DEFI project, there is space for everyone. One thing I’m almost certain of is that change is coming to the banking industry!

Lastly, crypto is risky. Nobody knows what is going to happen!

It’s not a bad idea to diversify, and a wonderful idea is affiliate marketing.

You can do it anytime, anywhere, around your schedule, in nearly any niche, with very low startup cost, and it can be a TON of fun.

I’ve been doing it for 15 years, and I’m giving away my system for FREE HERE.

I hope this blog post on the crypto project Aave was helpful. Bye for now.